")

- The Euro keeps the optimism well and sound vs. the US Dollar.

- Stocks in Europe keep the mixed note so far on Wednesday.

- EUR/USD briefly revisits the 1.0900 hurdle, as risk-on improves.

- The USD Index (DXY) surrenders further ground and retreats to 103.30.

- US, German yields rebound marginally ahead of further data results.

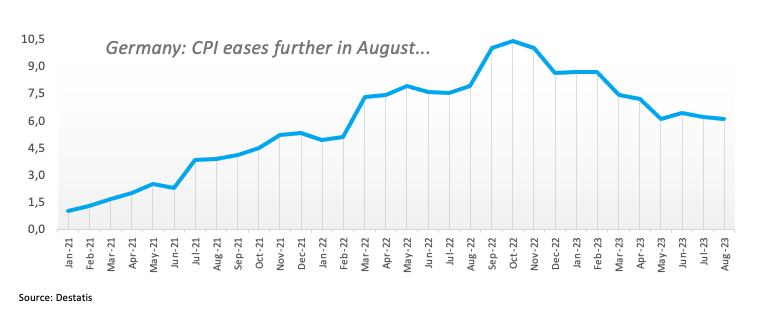

- Inflation in Germany is seen at 6.1% in the year to August.

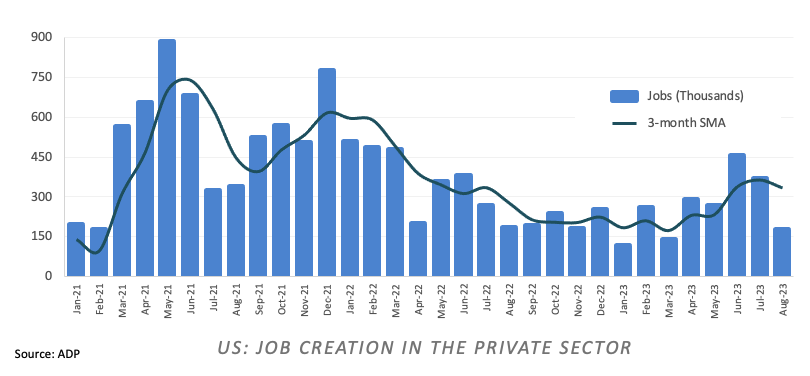

- US ADP report missed estimates at 177K jobs during last month.

The Euro (EUR) manages to reverse earlier losses vs. the US Dollar (USD), encouraging EUR/USD to regain upside traction and trespass the round level of 1.0900 in the European afternoon on Wednesday.

On the flip side, the Greenback succumbs to the persistent selling pressure and adds to Tuesday’s data-led sharp pullback, motivating the USD Index (DXY) to drop to multi-day lows near 103.20 ahead of the opening bell in Wall Street. The dollar’s price action, in the meantime, remains accompanied by a mild bounce in US yields across different maturities.

In the meantime, the Federal Reserve’s (Fed) tighter-for-longer approach now appears somewhat dented in response to recent data releases, which also pour cold water over expectations of a 25 bps rate hike at the November 1 gathering.

By contrast, there is no news around the European Central Bank (ECB) regarding its potential decision on rates once the summer season is over.

Data-wise in the region, flash inflation figures in Spain see the CPI rising 2.6% in the year to August, while Consumer Confidence in Italy receded a tad to 106.5 and eased to -16 when it comes to the broader euro area. In Germany, flash inflation figures now see the CPI rising at an annualized 6.1% for the current month.

In the US, the ADP report showed the private sector added 177K jobs in August (vs. 195K expected), while another estimate of the Q2 GDP Growth Rate expects the economy to have expanded 2.1% YoY and flash Goods Trade Balance predicts the deficit to have widened to $91.18B in July. Finally, Pending Home Sales will close the calendar.

Daily digest market movers: Euro finally hits the 1.0900 hurdle

- The EUR resumes the weekly uptrend vs. the USD.

- German and US bond yields pick up some fresh upside traction.

- Market participants will now shift their focus to the ADP results.

- JOLTs Job Openings dropped to the lowest level since March 2021 in July.

- The Fed’s tighter-for-longer narrative seems to be losing momentum.

- Investors see the Fed on hold for the remainder of the year.

- Further stimulus measures are likely to be taken by the PBoC in the near term.

- BoJ’s Tamura favoured the current loose monetary conditions.

Technical Analysis: Euro embarks on a test of 1.0930

EUR/USD’s weekly recovery faltered just ahead of the 1.0900 figure on Tuesday. The current upside momentum could leave further room for extra gains in the short term.

In case bulls push harder, EUR/USD is expected to face a minor resistance level at the weekly high of 1.0930 (August 22), which also appears reinforced by the provisional 100-day SMA. Further up comes the interim 55-day SMA at 1.0967, prior to the psychological 1.1000 barrier and the August top at 1.1064 (August 10). Once the latter is cleared, spot could challenge the weekly peak at 1.1149 (July 27). If the pair surpasses this region, it could alleviate some of the downward pressure and potentially visit the 2023 peak of 1.1275 (July 18). Further up comes the 2022 high at 1.1495 (February 10), which is closely followed by the round level of 1.1500.

The resumption of the downward bias could motivate the pair to revisit the August low of 1.0765 (August 25) ahead of the May low of 1.0635 (May 31) and the March low of 1.0516 (March 15). The loss of this level could prompt a test of the 2023 low at 1.0481 (January 6) to re-emerge on the horizon.

Furthermore, sustained losses are likely in EUR/USD once the 200-day SMA (1.0810) is breached in a convincing fashion.