Introduction

- “America First” and the rise of neo-mercantilism

Donald Trump’s 2024 campaign economic proposals focused on an “America First” strategy, reflecting key aspects of neo-mercantilism. This approach prioritizes boosting exports, reducing imports, and shielding domestic industries from foreign competition. It operates on the belief that international trade is a zero-sum game, where one country’s economic success comes at the expense of another.

- Adopting aggressive trade measures

Trump’s economic proposals align closely with neo-mercantilist principles, emphasizing protectionist measures such as high tariffs and supply chain reshoring. He has advocated for “universal baseline tariffs” on most imported goods, aiming to incentivize domestic production while imposing costs on foreign companies.

Additionally, he has pledged to revoke China’s Most-Favored-Nation trade status and gradually eliminate imports of essential goods from China over four years. He also proposes increasing tariffs on nations that manipulate their currency or engage in unfair trade practices.

- Shift toward aggressive neo-mercantilism

This shift from traditional free trade principles to a more assertive, nationalist trade approach has been described by analysts as “aggressive neo-mercantilism.” This strategy places a strong emphasis on prioritizing national interests, often at the cost of established global trade norms and international partnerships.

The modern-day iteration of aggressive neo-mercantilism represents a clear departure from collaborative global economic practices, moving towards a more isolated and competitive posture. This transformation could potentially reshape both the U.S. and global economies. Before exploring how this shift could unfold, it’s essential to trace the history of mercantilism, from its early roots to its contemporary applications.

Historical context and modern adaptation of mercantilism

- Mercantilism: Foundation of modern economic nationalism

Mercantilism was an economic theory and practice that shaped European trade and economic strategies from the 16th to the late 18th century. It emphasized that a nation’s wealth and power could be maximized by promoting exports while minimizing imports.

Countries following mercantilist policies focused on accumulating valuable resources like precious metals, establishing colonies, and securing monopolies over trade to ensure favorable balances of trade. To achieve this, they implemented measures such as imposing high tariffs, offering subsidies to local industries, and tightly controlling colonial markets.

Under mercantilism, governments played a significant role in economic affairs, driven by the belief that international trade was a zero-sum game—meaning one nation’s gain came at the expense of another. This approach contributed to the expansion of European colonial empires and influenced the global economic landscape, paving the way for industrial capitalism and modern economic nationalism.

- Neo-mercantilism and global market domination

Neo-mercantilism is a contemporary economic approach that draws inspiration from the mercantilist practices of earlier eras. It emphasizes state-driven strategies to secure trade surpluses and bolster national strength. In contrast to historical mercantilism, which often relied on colonization, neo-mercantilism employs more refined tactics, such as targeted tariffs, policies encouraging exports, and government backing for critical industries, to gain a competitive edge in global markets.

- Aggressive neo-mercantilism: A heightened economic strategy

Aggressive neo-mercantilism represents an intensified version of traditional neo-mercantilist policies, where a nation vigorously employs economic measures to advance its own interests, often at the expense of global trade norms and international partnerships.

This strategy typically involves strict trade protections, such as high tariffs and non-tariff barriers, aimed at protecting domestic industries from foreign competition. Additionally, aggressive neo-mercantilism might include the tactical use of currency manipulation and government subsidies to boost export competitiveness and limit the influx of imports.

This strong emphasis on national economic dominance often results in trade conflicts, strained diplomatic ties, and disruptions in global supply chains. By prioritizing national benefit over global collaboration, aggressive neo-mercantilism undermines the stability of the global economic system, potentially jeopardizing the interconnectedness of modern economies.

The following sections explore how the implementation of these neo-mercantilist policies could affect the U.S. economy, the global economy, international trade patterns, manufacturing, the growing trend of economic nationalism, relationships with key trading partners, global currencies, and commodity markets.

Implications for the US economy

- Economic protection vs. wider economic costs

Trump’s neo-mercantilist approach to the U.S. economy would likely have significant but mixed effects. On the positive side, the imposition of high tariffs and “America First” procurement policies could offer short-term protection and generate demand for certain U.S. industries (e.g., steel, aluminum, electronics assembly) by raising the cost of imported alternatives.

Trump argued that by increasing tariffs on foreign goods while reducing taxes for domestic producers, jobs and wealth could be retained within the country. Tariff revenues, in his view, could be directed towards domestic tax cuts—allowing for lower taxes on American workers and businesses. In theory, this “tax-for-tariff swap” might foster increased investment and job growth within protected sectors of the economy.

However, the broader economic costs to the U.S. would likely outweigh the immediate benefits. Tariffs, essentially taxes on imports, tend to increase costs for American consumers and businesses rather than foreign producers. Studies on Trump’s trade war from his first term indicate that the burden of these tariffs was primarily borne by U.S. consumers and firms.

For example, the National Retail Federation estimated that Trump’s proposed tariff package—which included a 10-20% blanket tariff on imports, alongside tariffs of 60-100% on goods from China—would result in an additional $46-78 billion in annual costs for American consumers. This would raise prices on everyday goods like apparel, toys, furniture, appliances, and footwear.

Such tariffs effectively function as a hidden tax, amounting to around $200–$300 per U.S. household annually in higher costs, according to the Tax Foundation. Tariffs enacted during Trump’s first term in 2018–2019 were described as “one of the largest tax increases in decades,” adding approximately $80 billion in new taxes for American households.

- Macroeconomic impact and supply chain disruptions

A tariff-focused policy is likely to have a negative macroeconomic impact on U.S. growth. Increased import costs contribute to higher inflation, which reduces consumers’ real purchasing power. Additionally, businesses, particularly manufacturers that rely on imported materials (such as machinery parts and specialized components), face rising operational expenses.

A 2019 study by the Federal Reserve found that the tariffs implemented under Trump’s administration led to increased input costs for U.S. producers, resulting in a decline in manufacturing jobs and an increase in prices. Although there were modest job gains in sectors shielded by tariffs, these were outweighed by job losses in other areas due to retaliatory tariffs and the higher cost of production.

A 2024 paper from the National Bureau of Economic Research (NBER), led by MIT economist David Autor, came to a similar conclusion. The research found that the 2018–2019 tariff conflict had no substantial impact on U.S. manufacturing employment. Meanwhile, foreign retaliatory tariffs negatively affected employment, particularly in agriculture, though this was somewhat offset by government subsidies for farmers.

Overall, widespread tariffs serve as a drag on economic growth. Trump’s new tariff proposals would likely increase costs and reduce U.S. GDP growth relative to the baseline. Additionally, the ongoing uncertainty surrounding trade policies and the disruption of supply chains could deter business investment. If companies anticipate a prolonged period of fluctuating tariffs and trade barriers, they may delay capital expenditures or decisions regarding relocation.

Financial markets could also respond negatively to the situation. The inflationary pressure caused by tariffs may prompt the Federal Reserve to maintain higher interest rates for a longer period, which would restrict access to credit and investment.

For instance, Oxford Economics revised its forecast for U.S. industrial output growth in 2025, reducing it from 2.1% to 1.1% due to the impact of Trump’s proposed tariffs, citing diminished business confidence and the slower pace of monetary policy easing.

- Economic trade-offs and potential benefits

Thus, while Trump’s mercantilist approach aims to boost American factories, it could also raise recession risks if escalating trade conflicts undermine consumer spending and corporate investment.

On the positive side, the U.S. government would collect significant tariff revenue (effectively transferred from consumers). Trump’s team projects trillions in revenue over a decade from a universal 10% tariff, theoretically offsetting other taxes. But this comes directly out of Americans’ wallets and from downstream businesses. If those funds are not perfectly redistributed (e.g. via tax cuts or subsidies to those hurt), the result is a net economic loss.

In sum, a neo-mercantilist second Trump administration might boost a few domestic industries and garner tariff revenues, but Americans broadly would likely face higher prices, retaliatory job losses in export sectors (like farming and aerospace), and slower growth relative to a free-trade scenario.

Implications for the global economy

- Economic downturn and supply chain disruptions

A significant shift by the U.S. toward mercantilist protectionism would create global economic ripples, typically hindering global growth. As the world’s largest importer, any major U.S. tariffs and efforts to replace imports would reduce demand for goods from other countries. This would likely slow growth in economies reliant on exports, from Asia to Europe.

During Trump’s initial trade conflict with China, both nations saw slightly reduced real incomes and GDP compared to what would have occurred otherwise. A second, more expansive trade conflict, especially if it expands beyond just the U.S.-China dispute to include North America and Europe, could have more severe effects.

- Revised economic forecasts and market instability

Global forecasters have started revising down their growth projections, anticipating the effects of renewed U.S. protectionism. In early 2025, in response to Trump’s tariff threats, Oxford Economics lowered its global industrial production growth forecast for 2025 by 0.5 percentage points. This revision reflects expectations that global tariffs, heightened policy uncertainty, and persistently high interest rates will dampen investment and manufacturing.

A surge in tariffs can act as both a negative supply shock—by driving up costs—and a negative demand shock—by reducing trade volumes—on the global economy. The IMF and other organizations have previously warned that a full-scale U.S.-China trade war could lead to a modest reduction in global GDP growth.

With the U.S. now targeting not just China but also its allies and neighboring countries, the overall impact could be substantial. If several major economies experience slower growth or mild recessions, the global economy could face significant headwinds.

- Decoupling and redefinition of supply chains

Trump’s goal to “completely eliminate U.S. dependence on China” and encourage American companies to reshore or “friend-shore” their production could accelerate the ongoing decoupling between Western and Chinese economic spheres.

This shift may lead to the creation of parallel supply chains—one centered around the U.S. and its allies, and another focused on China—replacing the previously interconnected global supply networks.

Such a transition is expected to drive up production costs worldwide, increase consumer prices, and lower corporate profit margins. Additionally, it could redistribute economic growth, potentially benefiting nations like Vietnam, India, and Mexico as investment moves away from China.

- Erosion of the multilateral trade system

The resurgence of mercantilism threatens to undermine the multilateral trading system that has supported global economic growth for decades.

In a potential second term, Trump’s administration could further sideline or diminish the influence of the World Trade Organization (WTO). Trump has consistently criticized the WTO and has already weakened it by blocking appointments to its appellate body.

Without a functional WTO to resolve disputes, the world could see an increase in retaliatory tariff conflicts, with no impartial authority to enforce international trade regulations.

- Geopolitical tensions and global market uncertainty

This climate of trade policy uncertainty, where tariffs can be imposed suddenly based on political motivations, can act as a significant barrier to global investment and innovation. Smaller nations, in particular, may face challenges as the U.S. and China engage in their competitive, zero-sum strategies. As one commentator noted, “middle and smaller nations are left with little choice but to follow suit or struggle” in such a hostile mercantilist environment.

In conclusion, Trump’s neo-mercantilist approach could result in a decline in global trade, disrupt supply chains, and inhibit global GDP growth. While some emerging markets might benefit from new manufacturing as production shifts, global business confidence and cooperation would likely decrease.

The world economy might enter an era characterized by “managed trade” blocks and slow economic growth—a significant departure from free trade, with protectionism increasingly justified on the grounds of national security.

Impact on global trade flows and trade policy

- Reorientation of trade flows

The second Trump administration is expected to significantly alter global trade patterns. One immediate consequence would be the redirection of U.S. imports away from countries targeted by tariffs.

If a universal tariff of 10–25% were imposed on most imports, it could lead to a reduction in total import volumes, with consumers and businesses turning to domestic products or sourcing goods from countries exempted from the tariffs.

Trump has indicated that tariff reductions might be offered to countries that engage in trade agreements or meet specific conditions, such as immigration or drug enforcement requirements, potentially sparing these allies from the full impact of the tariffs. Others, however, could face the full force of these trade measures.

- Trade diversion and shifts in manufacturing

This shift would likely drive trade diversion, with nations such as Vietnam, India, and Mexico potentially capturing a larger share of the market as U.S. importers look for alternatives to Chinese goods due to high tariffs. This trend was evident during the 2018–2019 U.S.-China trade conflict, where China’s proportion of U.S. imports declined, while other low-cost exporters, like Vietnam, saw significant increases in exports to the U.S. If Trump moves forward with his plan to gradually eliminate imports of Chinese “essential goods” over a four-year period, it could lead to a shift in the production of electronics, steel, and pharmaceuticals either back to the U.S. or to other countries not affected by U.S. tariffs.

At the same time, U.S. exports could also face redirection. China, for instance, has already reduced its reliance on U.S. agricultural products and may further cut back on purchases of American-manufactured goods. This could push U.S. exporters to explore alternative markets or increase their focus on domestic consumption.

- Consequences for global trade dynamics

Global trade flows are expected to shrink as a result of the imposition of tariffs and counter-tariffs by major economies, making certain trade exchanges unviable and leading to an overall decline in global trade volumes. The trade war between the U.S. and China, for instance, caused a significant reduction in trade that was not fully replaced by new partnerships, which hindered global trade growth in 2019. A broader escalation in trade conflicts could bring about a situation similar to the protectionist practices seen in the 1930s.

The structure of trade could evolve from multilateral agreements to more bilateral, transactional arrangements. Trump’s preference for one-on-one trade negotiations over large-scale multilateral deals might result in numerous bilateral talks, where the U.S. could push countries like the UK or Japan to make concessions in exchange for tariff exemptions.

- Unpredictability and politicization of trade policy

Global trade policy has become more unpredictable and politicized. Trump’s proposal for “reciprocal tariffs,” where the U.S. would impose tariffs equivalent to any foreign tariff, marks a shift away from stable, predictable tariff agreements toward a more reactionary approach.

Additionally, trade policy could be leveraged for broader political aims, such as Trump’s threats to impose further tariffs on Mexico and Canada unless they enhance border security or on China to push for changes in its trade practices.

The limited ability of the World Trade Organization (WTO) to enforce its rules, further weakened by the dysfunctional appellate body, has left few checks on nations pursuing such policies.

This situation could result in a shift toward managed trade and the formation of protectionist blocs, with the U.S. potentially challenging not only China but also its allies, each erecting barriers under the guise of fairness or security.

- Redesigning global trade maps

In essence, Trump’s aggressive neo-mercantilist approach would redraw global trade maps, favoring nations that align with U.S. demands and sidelining those that do not. This shift would generally diminish the efficiency and volume of international trade.

For example, after U.S. tariffs prompted China’s retaliation, Brazil emerged as China’s top soybean supplier, a change in trade flow that has solidified over the years. A similar redistribution could occur in manufacturing sectors; for instance, if U.S. tariffs make Chinese electronics uncompetitive in the American market, producers in Vietnam or Mexico might step in to fill the void.

However, such shifts require time and investment, and in the interim, supply bottlenecks or shortages of certain goods could disrupt production in various countries, highlighting the complex and often unintended consequences of aggressive trade policies.

US and global Manufacturing trends

- Revitalizing US Manufacturing

U.S. manufacturing would be a central focus of Trump’s policies, with the aim to rejuvenate domestic industry by protecting it from imports and incentivizing local production. Broad tariffs would initially boost some American manufacturers by making imported competing products more expensive. Trump claims his tariff-centric approach will “bring back millions of American jobs” and position America as a “manufacturing powerhouse like the world has never seen.”

In practice, these policies might prompt some companies to expand U.S. production to avoid tariffs, as seen during 2018-19 when foreign automakers and appliance makers increased their capacity in the U.S.

New government incentives for “reshoring” could further encourage the return of production, with proposals such as tax credits for companies relocating factories to the U.S. and denying federal contracts to firms that outsource to China.

- Challenges in Manufacturing employment

Despite these efforts, the overall trend in manufacturing employment may not align with the optimistic rhetoric. Advances in automation and productivity mean that even if factories return, they might employ fewer people than before.

Tariffs implemented in Trump’s first term raised costs for U.S. factories, reducing their competitiveness without significantly boosting job numbers. The 2024 Autor et al. study found that tariffs on Chinese goods had “no significant effect on U.S. employment” in manufacturing, while foreign retaliatory tariffs negatively impacted U.S. jobs, particularly in sectors like farm equipment manufacturing.

Rather than reshoring at scale, import sources shifted to other low-cost countries, sometimes leading U.S. firms to lay off workers or offshore operations to places like Vietnam to bypass tariffs.

- Global redistribution of Manufacturing

Globally, the redistribution of manufacturing might not result in a net increase but rather a shift in location. China, targeted by U.S. policies, might pivot from low-end export manufacturing to higher-tech industries and more self-sufficient domestic supply chains.

Labor-intensive manufacturing displaced from China could find new homes in developing nations like those in South/Southeast Asia. U.S. allies such as Mexico could benefit from near-shoring as companies could move production closer to the U.S. However, imposing tariffs on these allies negates these benefits.

- Sector-specific impacts and strategic focus

In specific sectors like steel and aluminum, Trump’s policies might temporarily boost domestic output. The proposed 25% tariff on all steel/aluminum imports could encourage U.S. mills to restart production, benefiting from higher domestic prices.

However, downstream industries such as automotive, aerospace, and construction would face higher material costs, potentially making their products less competitive and causing job losses.

Strategic industries such as semiconductors, pharmaceuticals, and electric vehicles might see targeted support through tariffs and government policies, possibly mirroring initiatives like Biden’s CHIPS Act and IRA, albeit framed differently.

- Outlook for global Manufacturing efficiency

In summary, the global manufacturing landscape under a resurgent mercantilism would likely be characterized by less integration and more duplication of efforts. The U.S. might see modest gains in output and capacity in protected sectors, but a broad-based revival of manufacturing jobs remains uncertain and historically unsupported.

Globally, manufacturing growth may realign towards countries exempt from U.S. tariffs or those benefiting from “friend-shoring,” while high-tariff targets like China might experience a slowdown in export-oriented manufacturing.

Overall, global manufacturing efficiency is likely to decline as companies restructure not for cost optimization but to navigate geopolitical barriers, reshaping the manufacturing sector under the influence of aggressive neo-mercantilist policies.

Impacts on global currencies

- Potential for a currency war

The revival of mercantilist policies under the second Trump administration will significantly influence currency markets, potentially igniting a currency war alongside the ongoing trade war. Historically, mercantilist-minded governments have favored a weaker domestic currency to boost exports. While the U.S. does not engage in explicit devaluation due to the dollar’s free-floating status, Trump has expressed frustration with a “too strong” dollar and suggested that the Federal Reserve might lower interest rates to weaken it.

Large trade deficits and new tariff barriers could lead to unpredictable fluctuations in the U.S. dollar (USD). In the short term, heightened global tensions and tariffs might paradoxically strengthen the dollar as a safe-haven asset, as investors typically turn to U.S. Treasuries and the USD during times of uncertainty. This reaction could ironically undermine some of the intended effects of tariffs by making U.S. exports more expensive globally.

- Intervention and responses

Trump might exert public pressure on the Federal Reserve for more accommodating monetary policy or might even consider direct intervention to depreciate the dollar’s value to support U.S. exporters. On the other side, the Chinese yuan (CNY) is likely to face downward pressure in response to escalating trade tensions. Anticipating U.S. tariffs, Chinese policymakers have considered allowing the yuan to depreciate to offset the impact on Chinese exporters.

- Impact on other currencies

Other Asian exporting countries, including South Korea, Taiwan, and Malaysia, might feel pressure to allow their currencies to weaken in order to stay competitive with a depreciating yuan, potentially leading to a wider currency conflict within Asia.

As for the euro (EUR), its impact would depend on Europe’s economic situation and the policy actions it takes. If U.S. tariffs cause economic stagnation in Europe, the European Central Bank might adopt more accommodative policies to boost growth, which could reduce the euro’s value. On the other hand, if Trump’s policies result in a slowdown in the U.S. economy, or if the Federal Reserve lowers interest rates, the dollar could weaken, potentially strengthening the euro.

- Currency market volatility

In summary, currency markets are likely to experience increased volatility. The EUR/USD exchange rate could fluctuate dramatically based on perceptions of which economy is suffering more from the trade disputes.

This environment of uncertainty and reactive policy measures could destabilize global financial markets, complicating efforts to predict currency movements and plan economic strategies.

Effects on commodities markets

(Energy, Metals, and Agricultural Goods)

- Energy sector impacts

A more protectionist Trump administration would have a significant impact on global commodities, including the energy sector, particularly oil and gas. Trump’s “energy dominance” strategy from his first term, which involved relaxing regulations on oil, gas, and coal and pulling out of the Paris climate agreement, led to record U.S. production and made the U.S. a net energy exporter for the first time in decades.

If these policies continue, it is likely that fossil fuel production will rise further, along with approvals for new pipelines and LNG export terminals, creating a favorable environment for oil and gas companies. This could put downward pressure on global oil and gas prices due to increased supply. However, U.S. exports of LNG to Europe and crude oil to Asia might rise, increasing competition in global energy markets.

On the other hand, Trump’s trade disputes could dampen global energy demand, particularly if tariffs and economic nationalism result in slower growth—especially in China, which is the world’s largest consumer of commodities.

- Metals and mining disruptions

Trump’s tariff-focused policies would have a direct impact on the metals sector, especially industrial metals such as steel, aluminum, copper, and rare earth elements. The administration’s goal of safeguarding U.S. metal industries by imposing tariffs (25% on steel and 10% on aluminum globally) may persist or even increase in the future.

In the short term, these measures could benefit U.S. steelmakers and aluminum producers, possibly encouraging more domestic mining of iron ore and bauxite. However, global metal prices could become more volatile, with U.S. prices likely increasing due to the tariffs, while an oversupply in international markets could lower prices elsewhere.

Over the long run, this might lead to shifts in production capacity. Foreign manufacturers may scale back output or explore alternative markets, while new production capacity could emerge in the U.S. if investors believe the tariffs will be sustained.

On the downside, industries in the U.S. that rely on these metals would face higher costs, which could diminish their global competitiveness and negatively affect sectors such as automotive and machinery manufacturing.

- Agricultural sector repercussions

The agricultural sector could face some of the most pronounced consequences of a trade conflict, as it is often the first target for retaliatory measures due to its political significance in the U.S. heartland.

For instance, when the U.S. imposed tariffs, China responded by placing a 25% tariff on American agricultural products like soybeans, corn, and pork in 2018. This led to a significant drop in U.S. exports to China, causing considerable losses for American farmers.

Should tariffs escalate further, countries such as Brazil and Argentina might take advantage of the situation by filling the void in China’s market. In fact, Brazil has already surpassed the U.S. as China’s top agricultural supplier.

Continued tariffs could provoke additional retaliatory actions, reducing U.S. farmers’ access to one of their key markets and potentially leading to oversupply of certain commodities within the U.S.

- Broader commodity market effects

Trump’s neo-mercantilist policies could likely heighten volatility in global commodity markets.

Energy markets may see a balanced supply, though demand growth could be more restrained, potentially keeping oil and gas prices stable unless major geopolitical disruptions occur.

The metals sector might face turmoil due to tariffs, which could push up domestic prices while causing oversupply in other regions.

Critical minerals could become a point of contention, especially if China responds by limiting exports of rare earths. This would drive up the costs of these essential materials, which are crucial for electronics and defense technologies.

Agricultural markets are likely to experience the most significant impact, with U.S. farmers potentially losing further global market share as retaliatory actions from trade partners lead them to secure food supplies from non-U.S. sources.

As economic nationalism continues to rise, even the movement of basic commodities might shift along geopolitical lines, creating new opportunities for some nations and challenges for others. This would likely contribute to increased volatility until a new trade equilibrium emerges.

Rise of economic nationalism worldwide

- Global shift toward economic nationalism

Trump’s neo-mercantilist policies reflect and contribute to a growing trend of economic nationalism worldwide. This shift has been amplified by recent events such as the COVID-19 pandemic and the intensifying rivalry between major powers. As a result, many countries are now focusing more on protecting domestic industries and securing supply chains, rather than prioritizing global market integration.

Should Trump return to the White House, it would further solidify this shift toward nationalist economic strategies, standing in stark contrast to the U.S.’s previous role as a champion of global free trade.

- Protectionism and global trade dynamics

The U.S., once a strong proponent of global free trade, has now adopted a stance that openly supports protectionism. This shift could inspire other countries to follow a similar path. In fact, this transformation is already in progress. As noted by The Diplomat, international trade is increasingly shifting “away from free trade and towards a more aggressive form of neo-mercantilism,” with both the U.S. and China engaging in tit-for-tat protectionist measures. For both Washington and Beijing, trade has become more than just an economic matter – it is now viewed as a strategic domain where tariffs symbolize not just trade barriers, but also power and national security.

- Impact on smaller nations and global trade policies

In an environment of rising competition and decreasing cooperation, smaller nations that once relied on a rules-based international trade system are now being forced to take defensive actions. These countries must either align with larger powers or face the risk of economic marginalization. For instance, India has responded by increasing tariffs and pushing for initiatives like “Make in India” to strengthen domestic manufacturing. Similarly, Russia has adopted import substitution strategies, even imposing tariffs on Chinese products to protect its local industries. Meanwhile, Europe is reassessing its approach, with a growing emphasis on “strategic autonomy,” more stringent foreign investment screening, and subsidies aimed at boosting the production of essential goods within the EU.

- Acceleration of nationalist trends under Trump

The second Trump term accelerates this global nationalist trend in several ways:

- Erosion of global trade norms: With the U.S. setting a protectionist example (and sidelining the WTO), other countries may feel free to ignore multilateral rules and raise their own barriers. We may see more trade wars among other pairs of countries, not just involving the U.S. (e.g. Europe and China have sparred over solar panels and may do more of that if norms weaken).

- Copycat tariff policies: Governments facing populist pressure might emulate Trump’s “tariff first” approach. For instance, a country suffering an influx of imports could impose Trump-like “reciprocal tariffs” or demand “fair trade” deals. The political narrative of putting one’s own nation first – even at the cost of global efficiency – is a powerful one that could resonate in many democracies and authoritarian states alike.

- National industrial planning: Economic nationalism often goes hand-in-hand with industrial policy. The U.S. under Trump uses tariffs plus incentives to boost domestic manufacturing. China has its state-driven industrial plans (Made in China 2025, etc.). Europe is responding with its own subsidies for green tech and semiconductors. As each tries to out-subsidize and protect their industries, we get a more fragmented global economy where state intervention in markets is routine.

- Geopolitical blocs: Economic alliances may align with geopolitical ones. We could see a U.S.-led bloc of like-minded nations that trade more freely with each other but maintain barriers against the “outside” (e.g. an expanded USMCA or allied network), while China leads its own sphere (deepening ties with willing partners via Belt and Road, RCEP, etc.). This bifurcation reinforces nationalist economic policies within each bloc, as they strive for self-sufficiency vis-à-vis the other.

Trump’s economic strategy reflects a broader global trend – a neo-mercantilist shift where nations focus on revitalizing their own industries and securing trade advantages, sometimes at the cost of global cooperation. This may lead to a rise in protectionist rhetoric, increased trade barriers, and a more tense international economic environment.

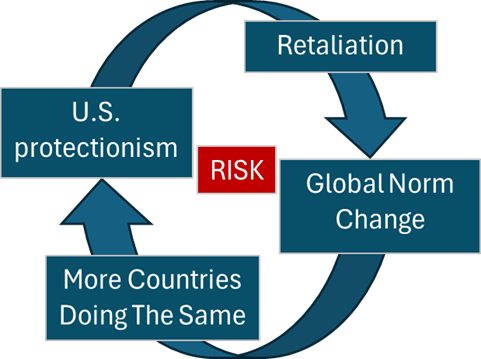

The danger lies in a self-reinforcing cycle: U.S. protectionist policies lead to retaliatory measures, prompting changes in global trade norms. As more countries adopt similar approaches, it creates a cycle of competitive economic nationalism that becomes increasingly difficult to undo.